Mortgage’s Second Act: The Fed’s Capital Overhaul and What Banks Should Do Now

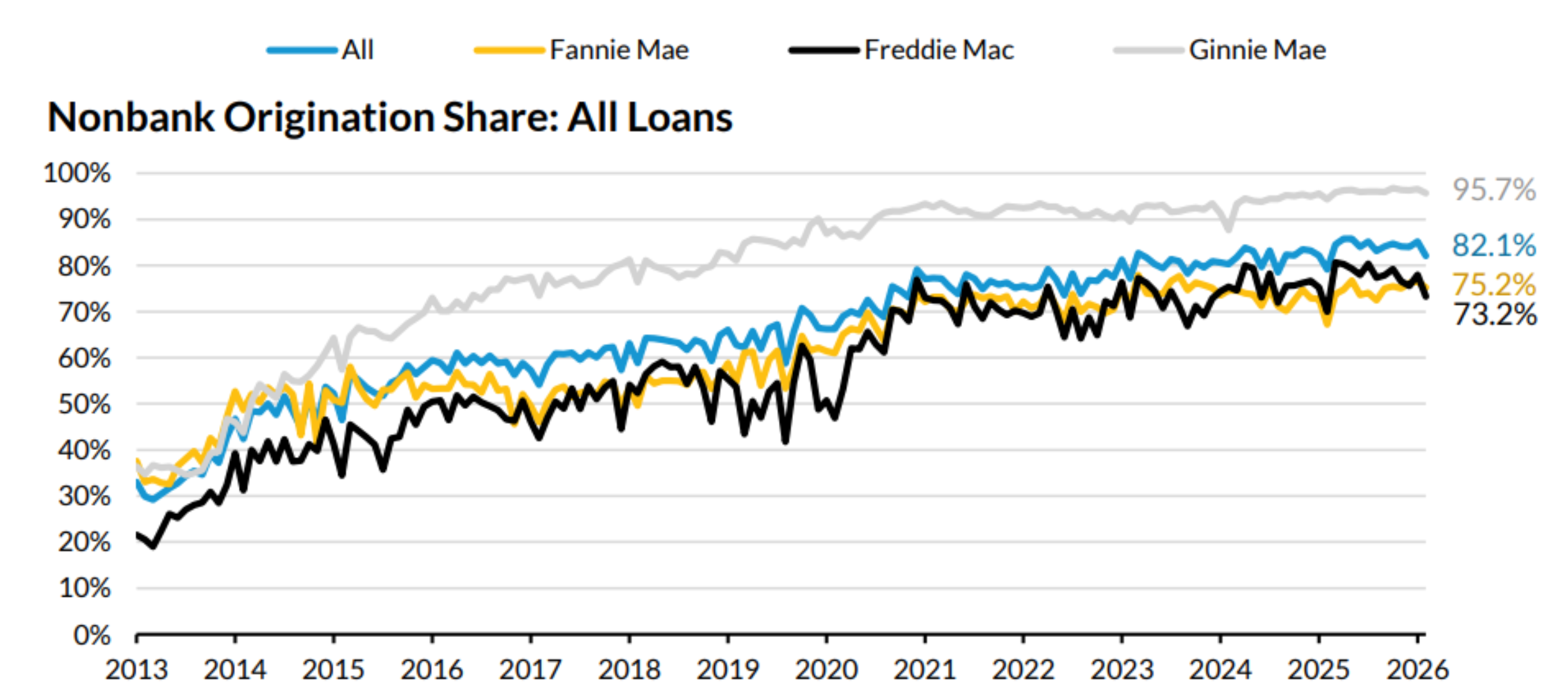

Traditional banks did not simply lose market share to independent mortgage banks; they chose to exit because the regulatory capital math made servicing economically punitive. As shown in the figure below, banks’ origination share of agency loans plummeted as nonbanks’ share surged from 30% in 2013 to over 82% by early 2026,[1] largely due to punitive capital treatment of mortgage servicing rights under Basel III.

Figure 1. Nonbank Origination Share: All Loans

Now the math is changing. The Federal Reserve, Office of the Comptroller of the Currency (OCC), and Federal Deposit Insurance Corporation (FDIC) recently issued proposed changes to the US capital framework that would materially revise the treatment of mortgage exposures and mortgage servicing assets.[2] For banks that withdrew from mortgage because the returns stopped justifying the capital drag, the proposal may reopen a business line many assumed no longer economically viable.

The Problem with the Old Rules

For much of the past decade, bank participation in mortgage origination and servicing has been shaped more by regulatory capital constraints than customer demand. The post-crisis framework—anchored in Basel III and implemented through US prudential rules—imposed particularly harsh treatment on mortgage-related exposures, most notably mortgage servicing assets (MSAs). While intended to enhance resiliency, the cumulative effect made mortgage a comparatively unattractive asset class from a return-on-capital perspective.

The MSA capital deduction framework sat at the center of this dynamic. Under the prior rules, MSAs were permitted only up to defined limits within regulatory capital, with any excess amount fully deducted from Common Equity Tier 1 (CET1)[3] rather than risk-weighted. For many institutions, these limits historically included a 10% individual threshold and 15% aggregate threshold under the original Basel III framework, later modified to a 25% threshold for certain banks under the 2019 capital simplification rule. This created a “cliff effect,” where incremental MSAs above the threshold triggered a disproportionate capital penalty.[4] In practical terms, once those limits were exceeded, additional servicing assets became economically unattractive to hold on a balance sheet, significantly reducing capital efficiency and constraining banks’ ability to scale servicing portfolios.

The implications were predictable. Banks—particularly regional and community institutions—began to scale back or exit mortgage servicing, often selling mortgage servicing rights (MSRs) to avoid capital drag. Simultaneously, mortgage origination strategies shifted toward “originate-to-sell” models, minimizing retained exposure. This resulted in a steady migration of mortgage servicing and origination capacity to nonbank financial institutions, which operate outside the same capital regime.

This structural shift reshaped the competitive landscape. Nonbanks—unencumbered by bank capital rules—priced more aggressively, invested in servicing platforms, and built scale. Meanwhile, banks ceded not only fee income but also a critical component of the consumer lifecycle relationship. What began as a capital optimization decision evolved into a strategic shift away from a core consumer product.

What Just Changed

The Federal Reserve, FDIC, and OCC March 2026 proposed revisions to the US capital framework introduce a meaningful recalibration of this dynamic. While the proposal spans multiple dimensions—including operational risk, market risk, and broader risk-based capital requirements—one of the most consequential anticipated changes for banks lies in the treatment of mortgage exposures and mortgage servicing assets. In particular, the proposal revisits the longstanding capital treatment of MSAs and introduces greater risk sensitivity into residential mortgage capital requirements, signaling a shift toward a more economically aligned framework for mortgage-related assets.

Most notably, the proposal eliminates the punitive MSA deduction framework in favor of a more traditional risk-weighted approach. Instead of being subject to threshold-based decisions, MSAs would instead receive a 250% risk weight. While still conservative, this represents a substantial improvement in capital efficiency relative to the current regime, particularly for institutions that would otherwise breach deduction thresholds.

Table 1. Simplified Example

| Current rules | Proposed framework | |

| MSA amount | $100 | $100 |

| Treatment | Full CET1 deduction | 250% risk weight |

| Risk-weighted assets (RWA) | $100 | $250 |

| Capital requirement | $100 | $20 |

| Capital impact | $100 CET1 deduction | $20 capital charge |

To illustrate the impact, consider a simplified example:

- Under current rules, a bank holding $100 of MSAs above the deduction threshold would see the full $100 deducted from CET1 capital.

- Under the proposed framework, that same $100 would instead be risk-weighted at 250%, resulting in $250 of risk-weighted assets (RWA).

- An 8% capital requirement translates to a $20 capital charge, materially lower than the $100 CET1 impact under full deduction.

While stylized, the example highlights the core shift: MSAs move from a binding capital constraint to a manageable (albeit still capital-intensive) asset class.

In parallel, the proposal introduces loan-to-value (LTV) sensitivity into residential mortgage risk weights, replacing the relatively blunt existing framework. Under the new standardized approach, lower-LTV mortgages receive more favorable risk weights while higher-LTV exposures are penalized. This aligns regulatory capital more closely with underlying credit risk and introduces greater differentiation across mortgage portfolios.

These changes do not exist in isolation but interact with broader elements of the Basel III Endgame proposal, including revised capital floors and expanded applicability of standardized approaches. For mortgage specifically, the direction is clear: a more economically rational and less distortionary capital treatment.

The Decision in Front of You

Banks are faced with a strategic question that many had effectively closed: Should we reenter or expand into mortgage origination and servicing? The answer is not uniform. Broadly, institutions fall into three distinct situations:

1. Banks that exited servicing and deemphasized mortgage

For institutions that sold MSRs and pivoted from mortgage, the proposed changes represent a potential reentry opportunity. The removal of the MSA deduction reduces the structural capital disadvantage that previously made servicing uneconomical. In theory, these banks can now compete more effectively on both pricing and retention.

However, reentry is not frictionless. Capabilities—technology, servicing infrastructure, hedging programs—have atrophied or been fully exited. For these institutions, the decision is less about capital relief and more about whether they are willing to rebuild an operating model in a market now dominated by scaled nonbanks.

2. Banks that maintained limited mortgage exposure

Other institutions retained some origination capacity but minimized servicing exposure. These banks often adopted a hybrid approach, participating in mortgage for relationship reasons while actively managing capital consumption.

For this cohort, the proposal creates opportunities to expand selectively, particularly in servicing. With MSAs becoming more capital efficient, these banks can reconsider the tradeoff between selling servicing rights versus retaining them for recurring fee income and maintaining close contact with the borrower. The introduction of LTV-based risk weights also allows for more granular portfolio optimization, favoring lower-risk segments without exiting the asset class entirely.

3. Banks with existing scale in mortgage

Finally, larger institutions with established mortgage platforms stand to benefit from improved capital efficiency at scale. For these banks, the question is more about optimization than reentry. Given the new rules, these banks can adjust their product mix, servicing strategy, and balance sheet allocation.

Yet scale does not eliminate complexity. These institutions still must navigate interactions with stress testing (e.g., Comprehensive Capital Analysis and Review or CCAR), interest rate risk in MSR valuations, and operational capacity constraints. The capital relief is meaningful but does not eliminate the need for disciplined risk management.

All three groups see a consistent theme: the competitive playing field is shifting but not uniformly leveling. Banks regain ground, but nonbanks retain structural advantages in cost and specialization.

What to Do Right Now

The current proposal is subject to a ninety-day comment period, after which final rules will be determined. While implementation timelines may extend over several years, the strategic implications will be immediate. Banks should treat this window as an active planning period, not a passive observation phase.

First, institutions should quantify the impact of the proposed changes on their capital position. This includes modeling the transition from MSA deduction to risk-weighting, assessing RWA sensitivity under different LTV distributions, and evaluating implications for CET1 ratios under both baseline and stress scenarios. This will require many banks to integrate mortgage-specific assumptions into broader capital planning frameworks.

Second, banks should revisit their mortgage strategy in a capital-informed context. This is not simply a question of “Can we reenter?” but rather “Where can we compete effectively given our balance sheet, cost structure, and customer base?” Scenario analysis—ranging from full reentry to targeted expansion—should be grounded in both financial metrics and operational feasibility. Reentry also could occur via an acquisition, so buy-versus-build considerations should be carefully evaluated.

Finally, institutions should consider engaging in the regulatory feedback process. The notice of proposed rulemaking explicitly invite industry input, and banks have an opportunity to shape final rule calibration, particularly around risk weights, implementation timelines, and transitional arrangements.

The key point will be timing: waiting for final rules may result in a lost first-mover advantage. Banks that begin modeling and strategic planning now will better position themselves to act decisively once the framework is finalized.

How BRG Can Help

Our professionals—including former regulators, bank executives, capital markets specialists, mortgage servicing experts, CPAs, and CFAs—have extensive experience helping financial institutions navigate complex regulatory change and translate it into actionable strategy.

We support clients with:

- capital impact modeling and Basel III endgame readiness, including MSA treatment, LTV-based RWA sensitivity, and CET1 optimization

- strategy and target operating development/implementation

- MSR valuation, hedging, and balance sheet integration

- regulatory interpretation and response support

- operational readiness assessments, including servicing platform evaluation and third-party oversight

- due diligence and merger integration support

BRG combines deep regulatory expertise with hands-on implementation experience to help banks align capital strategy with business opportunities. As the mortgage landscape evolves under the Basel III Endgame, institutions that move early and decisively will be best positioned to capture value.

[1] Urban Institute, Housing Finance at a Glance: A Monthly Chartbook, Housing Finance Policy Center (March 2026), p. 13. https://www.urban.org/sites/default/files/2026-03/March%20v4.pdf. See also: Government Accountability Office (GAO), “Nonbank Mortgage Companies: Ginnie Mae and FHFA Could Enhance Financial Monitoring,” GAO-26-107436 (February 2026).

[2] The Federal Reserve, OCC, and FDIC released three distinct proposals regarding regulatory capital rules on March 19, 2026. This analysis focuses exclusively on the proposed changes to Regulatory Capital and Standardized Approach for Risk-Weighted Assets (RWAs) under the Basel III Endgame framework.

[3] CET1 is the highest-quality regulatory capital, primarily composed of common shares and retained earnings, used to measure a bank’s solvency and ability to absorb losses under the Basel III framework.

[4] A full CET1 deduction is economically equivalent to a 1,250% risk weight, based on the 8% minimum total capital ratio (i.e., 100 ÷ 8% = 1,250%).

Related Professionals

Related Industries

Prepare for what's next.

ThinkSet magazine, a BRG publication, provides nuanced, multifaceted thinking and expert guidance that help today’s business leaders adopt a more strategic, long-term mindset to prepare for what’s next.