Mortgage’s Second Act, Part II: The New Borrower

Proposed changes to bank capital rules may make mortgages economically practical again for banks, but the market they would reenter has changed. Borrowers are more asset diverse, new structures such as crypto-backed financing are emerging, and underwriting and quality control may become more complex as a result.

What’s Happening

In Mortgage’s Second Act: The Fed’s Capital Overhaul and What Banks Should Do Now, we examined how proposed changes to bank capital rules may improve the economics of mortgage origination and servicing. This focused on whether changes to capital treatment—particularly the treatment of mortgage servicing assets—may reduce constraints that led many banks to step away from a business after the financial crisis.

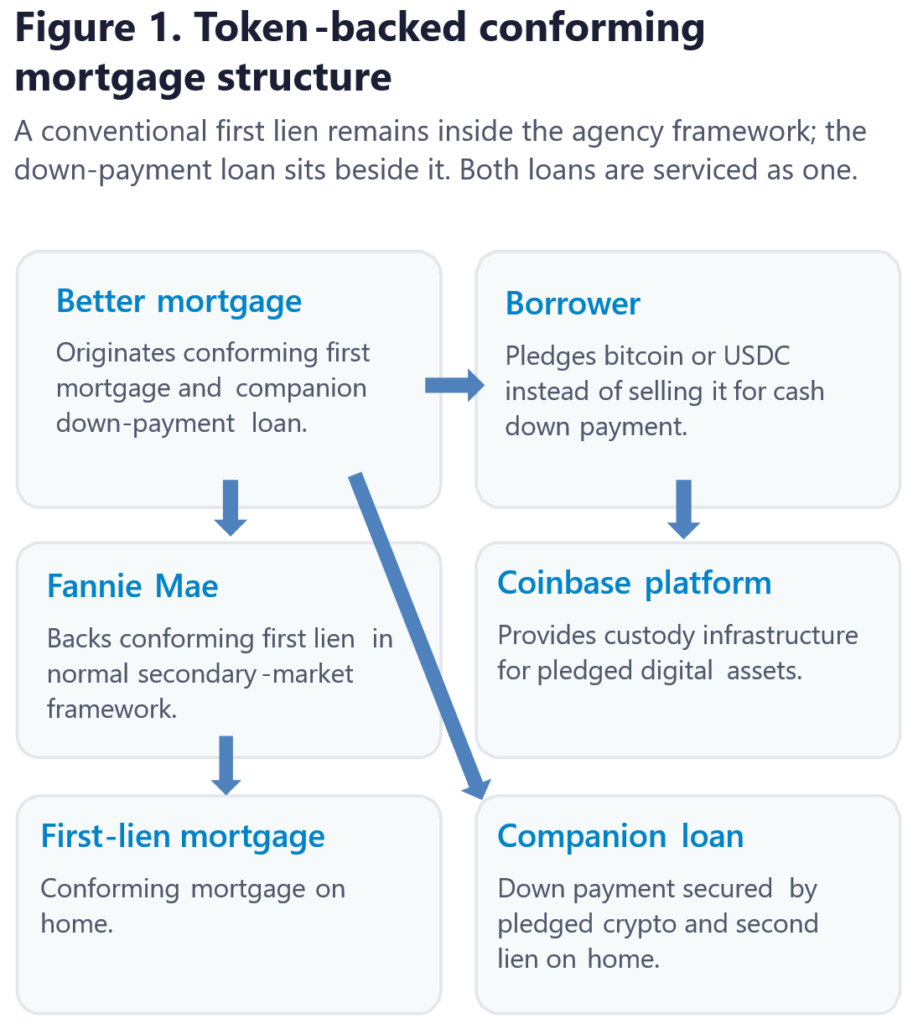

This follow-up article will explore the mortgage market that banks find themselves returning to today. Better Home & Finance (“Better”) and Coinbase recently unveiled a novel mortgage structure designed to fit within a Fannie Mae–backed conforming framework while allowing a borrower to pledge cryptocurrencies—specifically bitcoin or USD Coin (USDC)—to fund the down payment. This product, and others that are likely to follow, highlights a new borrower profile that does not fit cleanly within a traditional mortgage bank underwriting framework.

What Is a Crypto-Backed Mortgage?

The new conforming product offered through the Better/Coinbase partnership is not a case of Fannie Mae or any other government-sponsored enterprise (GSE) taking cryptocurrency onto its balance sheet. The crypto exposure isn’t moving at all. The structure is a two-loan transaction: a standard conforming first-lien mortgage on the home and a separate loan used to fund the down payment, secured by the borrower’s pledged crypto and a second lien on the property. Better originates both loans and holds the pledged crypto in custody on the Coinbase platform for the life of the down-payment loan.

At a basic level, the borrower is financing, not avoiding, the down payment. There are no margin calls if crypto prices decline, and liquidation risk arises only after a 60-day payment delinquency. If the home is sold, sale proceeds must be used to pay off both the first mortgage and the crypto-backed loan, after which the pledged crypto is released back to the borrower.

How the Structure Works

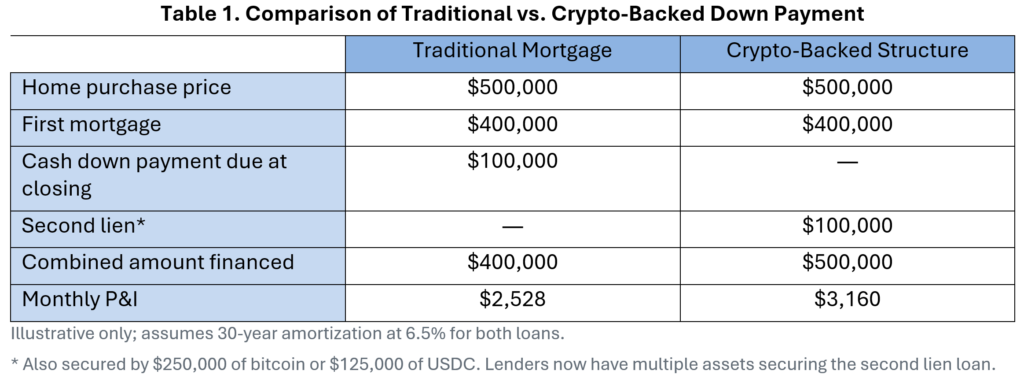

Assume a borrower is purchasing a $500,000 home and wants to make a 20% down payment. A traditional transaction would require $100,000 in cash and a $400,000 first mortgage. Under the Better/Coinbase structure, the borrower instead obtains a $400,000 conforming mortgage and uses a separate loan to fund the $100,000 down payment, secured by pledged bitcoin or USDC.

Both loans originate simultaneously, share the same interest rates and amortization terms, and are presented to the borrower as a single combined monthly payment. The pledged digital assets remain in custody for the duration of the down-payment loan or until that loan is repaid, with required collateral levels varying by asset type. For bitcoin, a 250% collateralization ratio applies, meaning the pledged asset must have a market value sufficient to meet that requirement at origination to support a $100,000 loan; USDC requires approximately 125%.

Using the Better/Coinbase structure, the borrower’s payment is presented as a single combined obligation even though it reflects two underlying loans. The comparison in Table 1 illustrates how the structure differs from a traditional cash down-payment mortgage.

While the monthly payment is presented as a single obligation, the borrower’s position is materially different. Equity at closing is replaced with leverage, while exposure to the underlying crypto asset is retained. Although the borrower’s payment goes up versus the traditional mortgage, they avoid a capital gain tax (generally 20% plus the 3.8% net investment income tax at the federal level plus any state tax) on the sale of the crypto and continue to gain economically from potential appreciation on the crypto asset. Depending on the borrower’s basis in the crypto asset and its future price gains, this could be significantly advantageous to certain borrowers.

The Evolving Borrower Profile

In the example above the borrower and non-depository crypto custodian retain market risk exposure; this highlights a broader shift in market dynamics. Both actors are willing to accept that exposure, whereas the traditional bank, or the GSE in this case, is not. The structure is attempting to bridge that gap.

In the example above the borrower and non-depository crypto custodian retain market risk exposure; this highlights a broader shift in market dynamics. Both actors are willing to accept that exposure, whereas the traditional bank, or the GSE in this case, is not. The structure is attempting to bridge that gap.

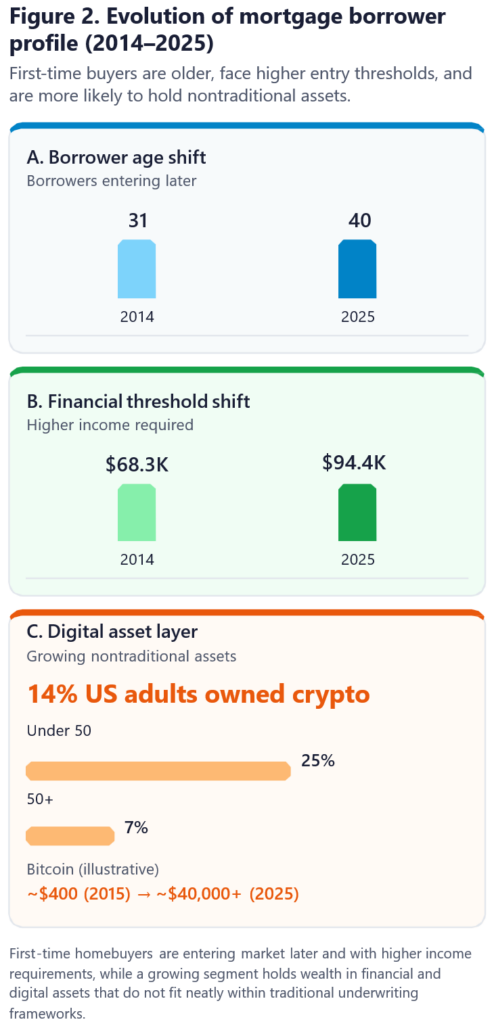

The borrower profile that banks will encounter today reflects that same shift. It is not the same profile many institutions left in the years following the financial crisis. As shown in Figure 2, the median age of first-time homebuyers increased from thirty-one in 2014 to forty in 2025. Median income increased from $68,300 to $94,400 (or about 38%), broadly in line with inflation. Housing costs, however, have risen 60% to 80%, meaning purchasing power has declined. This has resulted in an older borrower who is more likely to rely on accumulated assets to bridge the gap between income and cost of entry.

These trends point to three dynamics shaping the market today:

- Buyers are entering the market later.

- Housing costs are outpacing income.

- Balance sheets matter more at closing.

A growing portion of many borrowers’ balance sheets now sits in crypto-based assets. Gallup reports that 14% of US adults owned cryptocurrency in 2025, and Pew Research indicates that approximately 27% of adults under fifty have used cryptocurrency, compared with 8% of those over fifty. These assets are not central to every transaction but are increasingly part of the financial profile lenders must evaluate. Mortgage guidelines have long allowed financial assets to support a transaction, but typically only if they are liquidated or accessed through defined borrowing structures, such as a permitted 401(k) loan or documented withdrawal. Crypto-backed mortgage products do not change those rules but instead allow the borrower to retain exposure to the asset while using it to support the transaction.

What This Means for Underwriting

As the borrower profile changes, so will underwriting. The first lien may still be conforming, but the credit decision is no longer based on the mortgage alone. When the down payment is financed, the borrower qualifies with a higher payment and a more leveraged balance sheet than in a traditional cash-down transaction.

That difference appears first in debt-to-income (DTI) ratio. In a traditional structure, a $400,000 mortgage at 6.5% produces a principal-and-interest payment of $2,528. Under the combined structure, that increases 25% to $3,160. Maintaining the same DTI requires higher qualifying income or less other debt.

What appears to be a conventional transaction introduces three distinct underwriting challenges:

- Higher payment burden: The borrower must qualify with a larger monthly obligation for the same home purchase.

- Higher leverage: The transaction adds $100,000 in subordinate financing, increasing combined leverage to 100% because the down payment is financed rather than contributed in cash.

- Reduced liquidity: The pledged crypto remains on the balance sheet but is encumbered as collateral, reducing available liquidity and reserves.

Structures of this type have a limited performance history, while traditional underwriting models are built on decades of data. Here the borrower profile reflects a more leveraged structure combined with an asset that is volatile and relatively new in mortgage finance. While the first lien may still meet conforming standards, the combined structure introduces variables not fully captured in historical performance data, placing greater reliance on underwriting judgment.

Adapting to a Changing Borrower and Market

The borrower profile is evolving beyond housing finance. This is not just a mortgage issue. Banks are seeing similar dynamics on the deposit side, where attracting younger customers has become more challenging as their assets and financial behaviors move outside traditional banking channels.

Mortgage history is full of products that looked rational at launch but far riskier once they reached scale. Interest-only loans, payment-option adjustable-rate mortgages, and low-documentation products were all introduced with credible business logic, yet regulators warned that such structures could obscure repayment risk, create payment shock, and weaken underwriting discipline, particularly when risks were layered together. Mortgage innovation is ultimately judged under real operational stress.

To compete in today’s market, banks will need to engage a borrower with a different balance sheet. The Better/Coinbase structure points to one possible path: keep the first lien inside a conforming framework while placing the crypto-backed loan and custody mechanics outside the GSE credit box. That would allow participation without direct crypto exposure, provided third-party relationships are properly structured and governed.

The real test comes after origination. While subordinate financing is permitted, the operational reality changes when that financing is tied to pledged crypto and serviced as a single payment stream. In practice, this introduces new control points:

- Payment processing: one borrower payment allocated across two legal obligations

- Servicing mechanics: payoff, remittance, and collateral released across both loans

- Custody integration: digital-asset custody events aligned with borrower status

- Default timelines: crypto liquidation and foreclosure may run in parallel

- Investor reporting: first-lien reporting remains compliant while companion-loan activity is tracked separately

These dynamics extend directly into prefunding quality control (QC), post-closing QC, and default servicing. They do not simply add operational steps but instead increase the complexity of servicing, investor accounting, and regulatory oversight at the same time. They also will draw closer attention from regulators, particularly at the state level, as these structures move beyond early adoption.

Conclusion

The potential return of banks to mortgage is driven in part by changes in capital treatment, but the more important shift is occurring on the demand side. Borrowers are arriving with different balance sheets, expectations, and relationships with the traditional banking system. Products like crypto-backed mortgages are emerging and reflect a broader movement toward recognizing forms of wealth that do not fit neatly within established frameworks.

Banks cannot evaluate mortgage in isolation. The same borrower profile shaping mortgage demand is evident on the deposit side, where institutions already face challenges attracting younger customers. This is not simply a product issue. Institutions that recognize this structural shift and adapt how they underwrite, structure, and service these relationships will be better positioned than those that do not.

How BRG Can Help

BRG helps banks, mortgage companies, and other financial institutions translate market change into operating decisions that are commercially useful and regulatorily defensible. These include capital-impact assessment, mortgage strategy, target operating model development and implementation, underwriting framework design and risk modeling, model-risk governance, QC enhancement, servicing and investor-readiness reviews, third-party oversight, and targeted reviews of newer structures that combine conventional mortgage products with adjacent financing or nontraditional assets.

Related Professionals

Related Industries

Prepare for what's next.

ThinkSet magazine, a BRG publication, provides nuanced, multifaceted thinking and expert guidance that help today’s business leaders adopt a more strategic, long-term mindset to prepare for what’s next.