SBA Citizenship Eligibility Changes: Implications for Lenders and Operational Considerations

BRG is home to renowned thought leaders and experts considered authorities in their fields of work. Our timely research and perspectives provide analysis and insights on the most important issues facing the industries and organizations we serve.

What Has Happened

On February 2 and March 6, 2026, the US Small Business Administration (SBA) issued policy notices banning non-US citizens, foreign nationals, and US citizens or nationals living outside of the United States or its territories from accessing certain SBA-guaranteed small business loans. Under the SBA’s new policies, only small business owners (direct and indirect) who are US citizens or US nationals with their principal residence in the United States are eligible for SBA’s 7(a) and 504 loan programs and its Microloan and Surety Bond Guarantee programs. This differs from the SBA’s previous policy, which allowed foreign nationals, permanent residents (i.e., Green Card holders), and US citizens or nationals with principal residence outside of the United States to have majority ownership in small businesses receiving SBA loans.

High-level changes to SBA’s lending eligibility requirements are shown below:

| Previous Requirements | New Requirements |

| US citizens and lawful permanent residents (domestic and abroad) eligible | Only US citizens or US nationals with principal residence in US eligible |

| Certain foreign ownership allowed | No foreign ownership permitted |

Effective Dates:

-

- SBA 7(a) and 504 programs: March 1, 2026

- Microloan and Surety Bond Guarantee programs: April 1, 2026

- Grandfathering cutoff: Applications for microloans or surety bonds currently “in process” are protected only if they receive an official SBA loan or bond guarantee number within thirty days after publication of the notice.

- Existing 7(a) and 504 loans: Policy notices do not retroactively change the status of existing 7(a) or 504 loans issued before March 1, 2026.

Issuance of SBA policy notices and guidance is not uncommon. However, these changes to loan eligibility and the effective dates have the potential to create operational, underwriting, and compliance implications for SBA lenders. Lenders’ ownership verification and borrower eligibility screening processes may need to be revised to confirm citizenship for all proposed owners of a small business applicant. Additionally, while the SBA has made an applicant’s immigration status a dominant eligibility factor, lenders should review their decisioning practices and data for potential increased compliance risks related to the Equal Credit Opportunity Act (ECOA) and its implementing regulation (Reg. B), which prohibits discrimination based on protected classes such as national origin or race.

Financial institutions need to review their product offerings, policies, underwriting practices, and reporting for alignment with the SBA’s updated policies, all federal and state regulatory requirements, and potential portfolio impacts.

Potential Lender Impacts

Eligibility Criteria and Verification

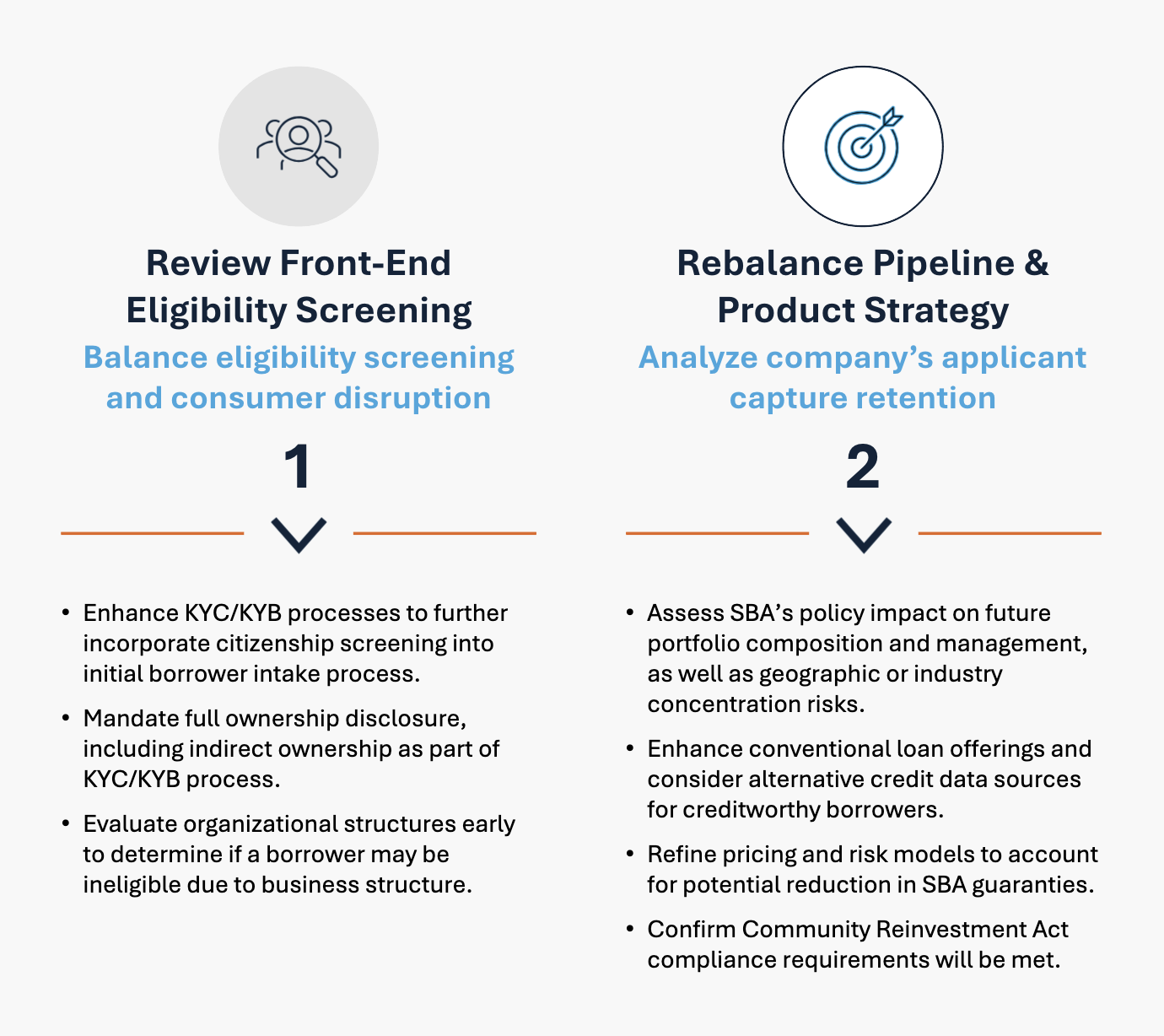

SBA loan applicants must meet certain eligibility requirements, such as financial size, business type, and demonstration of reasonable ability to repay a loan.[1] With the new policy requirements, all business owners must also provide proof of US citizenship and permanent residence within the United States. The changes to eligibility criteria will need to be included in underwriting processes, and loan officers may need to consider other loan products for previously eligible applicants who are now ineligible for SBA loans, which could result in pipeline disruptions or borrower restructuring requests. To meet SBA requirements and other business demands in a competitive landscape, lenders may need to update underwriting criteria and reporting and consider offering alternative credit products to meet customer needs.

Know Your Business (KYB)/Know Your Customer (KYC) Screening

While financial institutions verify business ownership and certain beneficial ownership percentages for KYB/KYC requirement adherence and sanctions screening, verifying citizenship has not historically been explicitly required.[2] Complying with SBA’s new citizenship requirements may entail implementing additional applicant/ownership verification steps to confirm eligibility; applicants previously eligible for SBA financing may now be ineligible. Pending an executive order requiring verification more broadly, loan officers may consider other loan products for their customers to meet demand from this population.

Loan Pipeline Impacts

With competition for loans between traditional financial institutions and fintechs on the rise, product availability for lenders’ target customers is critical. To minimize potential pipeline impacts, lenders with significant SBA loan portfolios may choose to develop other private products for applicants who do not meet the new eligibility requirements. This may require additional costs—such as additional employee training and coaching, marketing, and other operational changes—that need to be balanced against lender portfolio metrics, compliance and risk management policies, and lenders’ strategic objectives.

Credit Profile Risk Management

Notable declines in SBA-guaranteed financing could shift the market toward increased risk within institutions’ conventional lending portfolios. Without credit enhancement provided by SBA guarantees, institutions may need to recalibrate their risk tolerance and re-forecast for potential portfolio shrinking as borrowers may be less inclined to pursue private loans.

Lenders’ focus will continue to include:

- stability and predictability of cash flows

- strength and liquidity of sponsors

- availability of collateral and secondary repayment sources

Early stage companies and asset-light businesses that have historically relied on SBA programs to access credit will likely experience the most impact.

Lenders engaged in small business lending may consider reviewing their loan portfolios and target lending areas to assess if a future shift in risk composition is probable due to a reduction in available SBA-backed financing. Other steps may include evaluation of existing credit policies, risk rating frameworks, and concentration limits, as well as evaluation of risk-based pricing tiers and inclusion of alternative credit data.

Compliance and Operational Adjustments

The updated SBA eligibility requirements necessitate targeted changes across lender operations, underwriting workflows, and compliance controls. Institutions must ensure that eligibility determinations are consistently applied and well documented throughout the loan lifecycle.

Key areas include:

- Marketing updates: update or remove marketing materials that include outdated SBA eligibility requirements to avoid consumer confusion.

- Intake and pre-screening: enhance front-end processes to identify ineligible ownership structures early and reduce pipeline disruption.

- Origination and underwriting training: update training communications to inform lending and credit teams of the revised product requirements with reminders of fair lending compliance standards.

- Ownership verification documentation: strengthen requirements to evidence both direct and indirect ownership as required by the SBA.

- Consumer privacy protections: reinforce consumer privacy controls and protocols related to the collection, storage, use, and disposal of applicant citizenship information and documentation.

- Policy and system updates: revise internal credit policies, SBA eligibility checklists, loan operating systems that capture and analyze ownership percentages and eligibility criteria, related controls and reporting updates, and procedures to reflect current standard operating procedure requirements.

Given the SBA’s continued emphasis on eligibility compliance, ownership verification remains critical. Insufficient diligence or documentation may increase the risk of guaranty repair or denial, as well as findings during SBA lender reviews.

What Lenders Can Do: Action Items

The new eligibility requirements represent a shift in origination, underwriting, and compliance. Adopting the requirements early can improve pipeline productivity and minimize disruption.

[1] SBA, “Loans: 7(a) Loans: Am I eligible?” (accessed April 1, 2026). See similar sections for 504 loans and Microloans.

[2] At the Semafor World Economy Summit, US Treasury Secretary Scott Bessent made public comments that an executive order to require banks to collect citizenship information on their customers is “in process.” Mueller, Eleanor, and Ben Smith, “Exclusive / Bessent: US should ‘wait and see’ before lowering interest rates,” Semafor (April 13, 2026).

Prepare for what's next.

ThinkSet magazine, a BRG publication, provides nuanced, multifaceted thinking and expert guidance that help today’s business leaders adopt a more strategic, long-term mindset to prepare for what’s next.