Dire Straits: The Hidden Supply Chains of the Strait of Hormuz

Oil may dominate headlines, but LNG, helium, fertilizers, and petrochemical feedstocks moving through the Strait of Hormuz could transmit shocks from global industry to food security—and ultimately lead to geopolitical instability—within two to three quarters.

Summary

We recently described the current geopolitical environment as one defined less by isolated disruptions than by stacked constraints: overlapping pressures across shipping, export controls, financial networks, and trade policy that collectively reduce the reliability of global value chains. The ongoing situation in the Strait of Hormuz illustrates how quickly those constraints can compound when a critical logistics corridor sits at the intersection of energy, industrial, and agricultural supply chains.

Hostilities in and around the strait raise the possibility that one of the world’s critical maritime corridors could remain operationally constrained for an extended period. Much public discussion has focused on implications for oil markets, but crude is only one of several strategic commodities that transit the strait. Liquefied natural gas (LNG), helium, liquefied petroleum gas (LPG), refined fuels, petrochemical feedstocks, and fertilizers also move through in significant volumes. Disruption to these flows—whether through direct conflict, maritime mines, attacks on merchant vessels, or prohibitive insurance conditions—could propagate through industrial supply chains well beyond the energy sector.

The most consequential effects may not appear immediately. Instead, they will likely emerge gradually as stacked constraints reduce shipping reliability, increase input costs for fertilizers and chemicals, and ultimately affect agriculture, manufacturing, and consumer markets two to three quarters later.

The chokepoint that amplifies constraint

When discussing the Strait of Hormuz, conversations usually begin and end with oil. The corridor is widely recognized as one of the most important energy chokepoints in the world, carrying a substantial share of global petroleum flows from the Persian Gulf to international markets. But focusing solely on crude oil risks missing the broader structural importance of the strait.

In reality, the Strait of Hormuz functions as a multicommodity industrial corridor linking Gulf energy and chemical production to global markets. In addition to crude oil, the passage carries large volumes of LNG, helium, LPG, refined petroleum products, petrochemical feedstocks, and fertilizers.

These materials sit at the base of multiple industrial supply chains. Disruptions in the corridor therefore propagate beyond energy markets into agriculture, manufacturing, transportation, high technology, healthcare, research sectors, and consumer goods production.

Viewed through the lens of value‑chain risk management, the Strait of Hormuz is more than a geopolitical flashpoint. It is a constraint amplifier.

Because so many upstream industrial inputs move through the same corridor, disruption in the strait can propagate across multiple supply chains simultaneously—a classic example of stacked constraints emerging in real time.

Why duration matters more than the initial shock

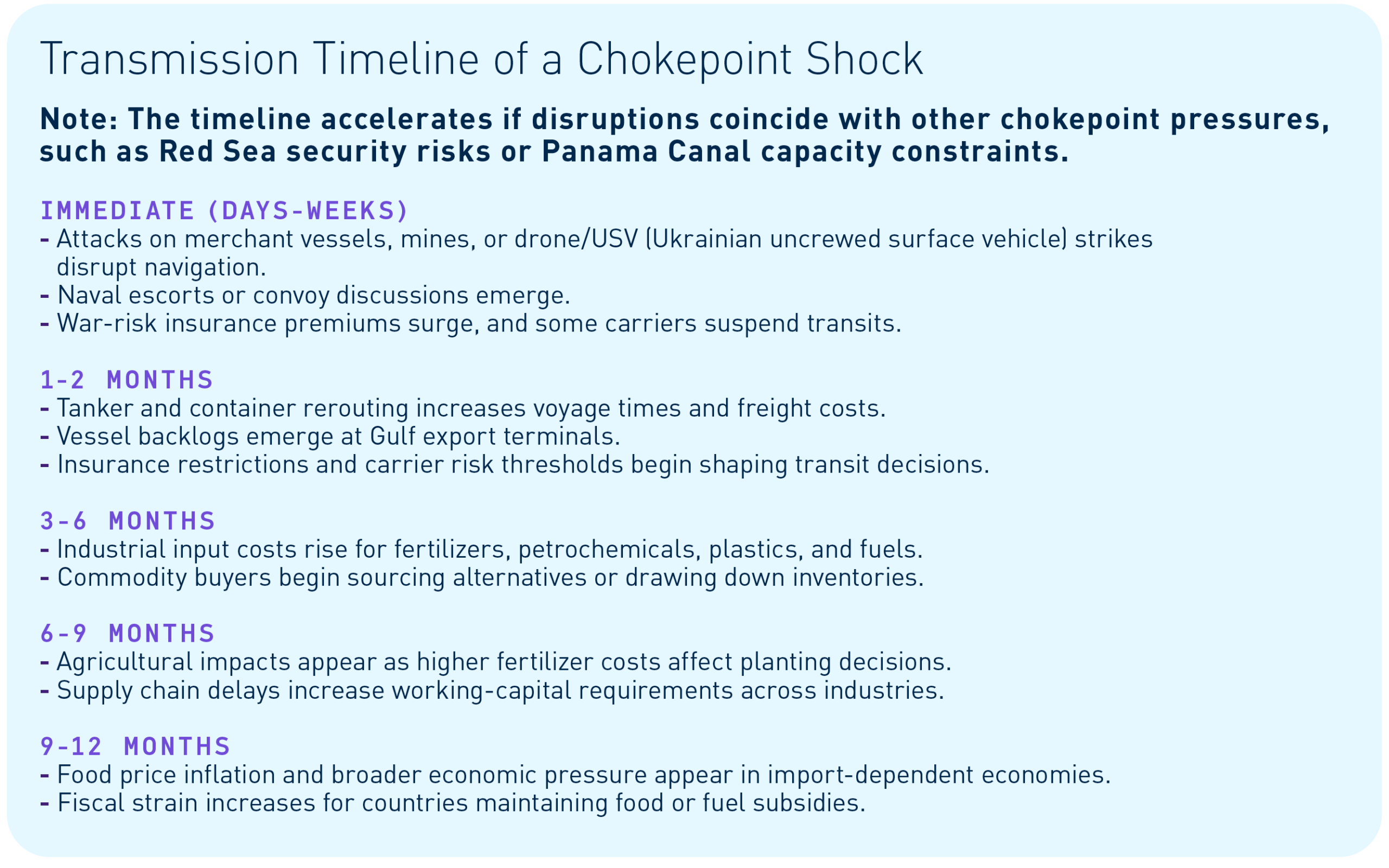

The situation in and around the Strait of Hormuz has moved beyond the early phase of a hypothetical disruption. Since late February, attacks on merchant vessels, maritime mines, and drone or unmanned surface vessel strikes have introduced direct operational risk the corridor.

In the immediate aftermath of such events, markets typically react first. Energy prices move quickly, insurers reassess war-risk premiums, and carriers apply surcharges or alter routing decisions.

Operational behavior on the water also begins to change. Some vessels reduce broadcast activity on the Automatic Identification System (AIS), while others alter transmitted vessel identity or ownership information to reduce perceived targeting risk. These adjustments complicate maritime tracking and traffic management and introduce additional uncertainty for carriers, insurers, and port operators assessing the safety of transit through the corridor.

Vessels operating in and around the Gulf have reported episodes of Global Positioning System (GPS) or broader Global Navigation Satellite System (GNSS) interference, which can degrade navigational accuracy and disrupt positioning systems used for collision avoidance, port approaches, and restricted navigation. In heavily trafficked waters such as the Strait of Hormuz, these disruptions increase operational risk and further complicate routing decisions for ship operators and maritime authorities. When GPS interference coincides with reduced AIS broadcasting, the ability of vessels and traffic management systems to maintain situational awareness deteriorates, increasing collision risk in one of the most congested shipping corridors in the world. Additionally, this loss of situational awareness increases the risk of a violation of a country’s territorial waters, often a trigger event for a political or military response, or both.

Real-time maritime tracking platforms show vessels loitering outside the Persian Gulf or delaying entry from the Gulf into the Strait of Hormuz while awaiting clearer security conditions or potential naval escort windows. This pattern of staging and delayed transit increases voyage times, contributes to congestion near Gulf export terminals, and is an early indicator that commercial operators are adapting navigation practices to a contested maritime environment.

The problem changes character as the conflict persists, however.

What initially appears as a market shock gradually becomes an operational constraint. Carriers adjust schedules, insurers tighten underwriting standards, and some operators limit exposure to higher-risk corridors. Transit times lengthen as vessels slow, reroute, stage outside the corridor, or wait for naval escorts, while ports and export terminals begin to experience congestion.

At that point, duration becomes the critical variable. The longer a contested maritime environment persists, the more likely that commercial behavior will begin to shift across the logistics system. Inventory buffers shrink, and working-capital requirements rise as cargo spends more time in transit.

Over time, volatility evolves into backlog, backlog into scarcity, and scarcity into broader economic pressure across multiple sectors.

Therefore, the key analytical question is not simply whether conflict occurs in the corridor, but how long global trade must operate under those conditions.

Even when naval escorts preserve the physical movement of vessels through the strait, sustained maritime risk can still degrade the reliability of shipping, insurance, and financing networks that underpin global trade.

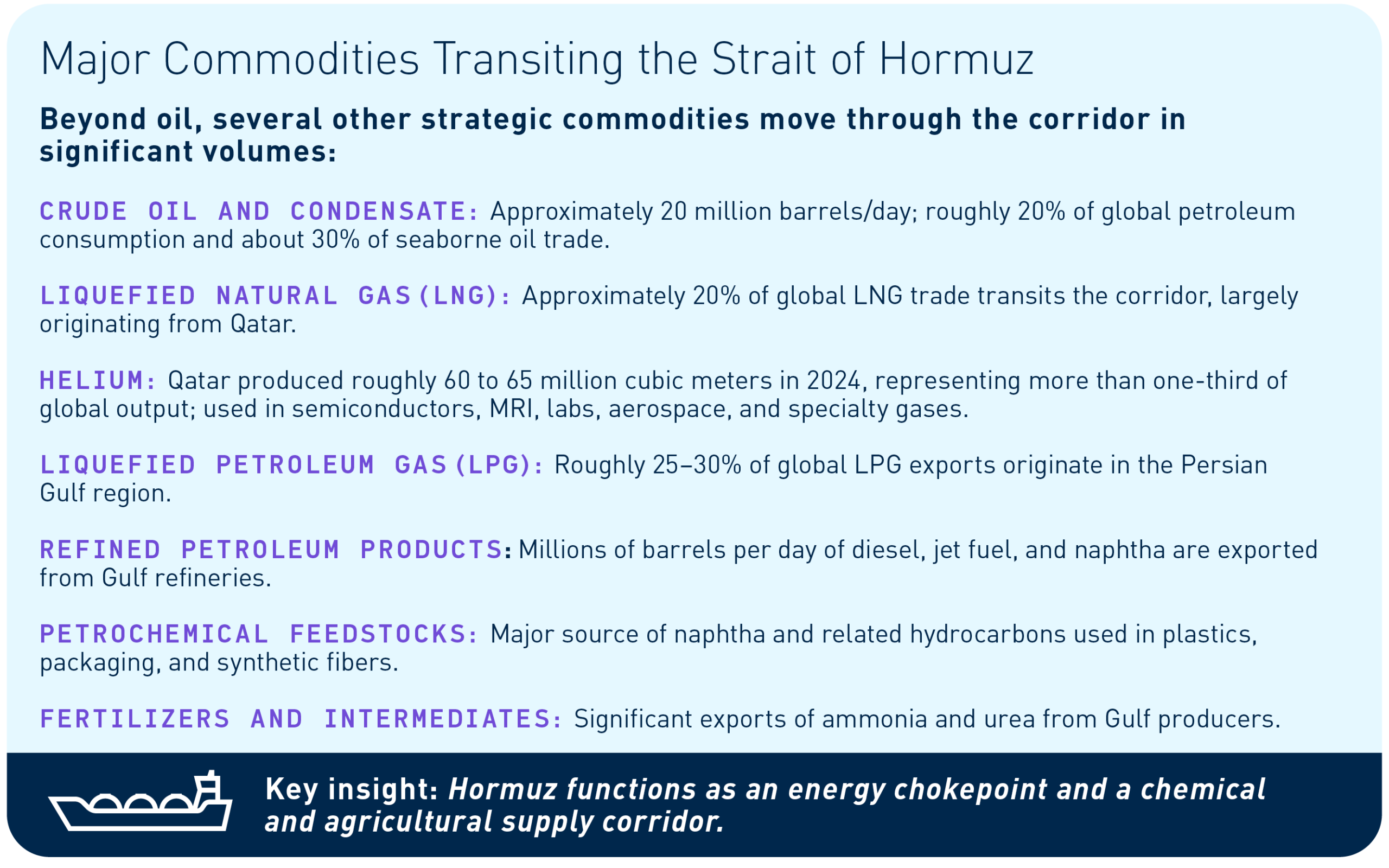

The commodities at risk

Oil dominates public discussion, but several other commodities transiting the Strait of Hormuz are equally important to global industrial production.

LNG

A substantial portion of the world’s LNG exports originates in Qatar and must pass through the strait. Natural gas is not only a fuel but also the primary feedstock for ammonia production.

Helium

Helium is a small-volume but strategically critical industrial gas, essential for semiconductor manufacturing, MRI systems, scientific instrumentation, and aerospace applications. A large share of global supply originates in Qatar’s Ras Laffan gas-processing infrastructure.

LPG

The Gulf region is a major exporter of LPG, which serves both household energy markets and petrochemical manufacturing.

Refined petroleum products

Diesel, jet fuel, and naphtha move through the corridor in large volumes. Diesel is particularly important because it underpins freight transportation, mining operations, and agricultural equipment.

Petrochemical feedstocks

Naphtha and related hydrocarbons from Gulf refiners are critical inputs for the production of plastics, synthetic fibers, packaging materials, and other industrial products.

Fertilizers and fertilizer intermediates

The Persian Gulf region exports significant quantities of ammonia and nitrogen fertilizers, such as urea, both of which are essential inputs to global agriculture.

Together, these materials form part of the industrial substrate of the modern economy. Disruption in their movement can ripple simultaneously through agriculture, manufacturing, logistics, and consumer goods production. These commodities represent the upstream inputs for several of the world’s most important industrial and agricultural supply chains.

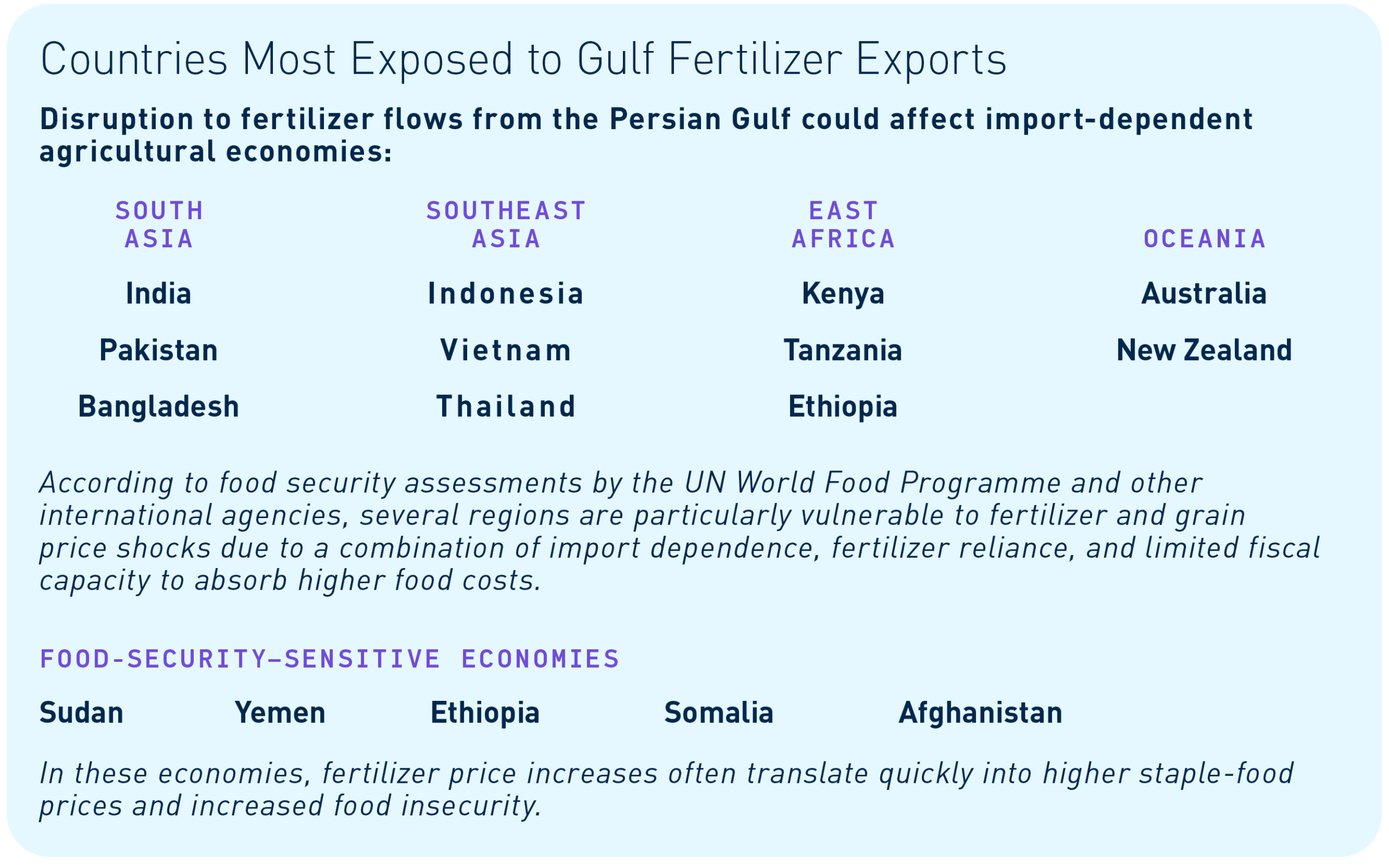

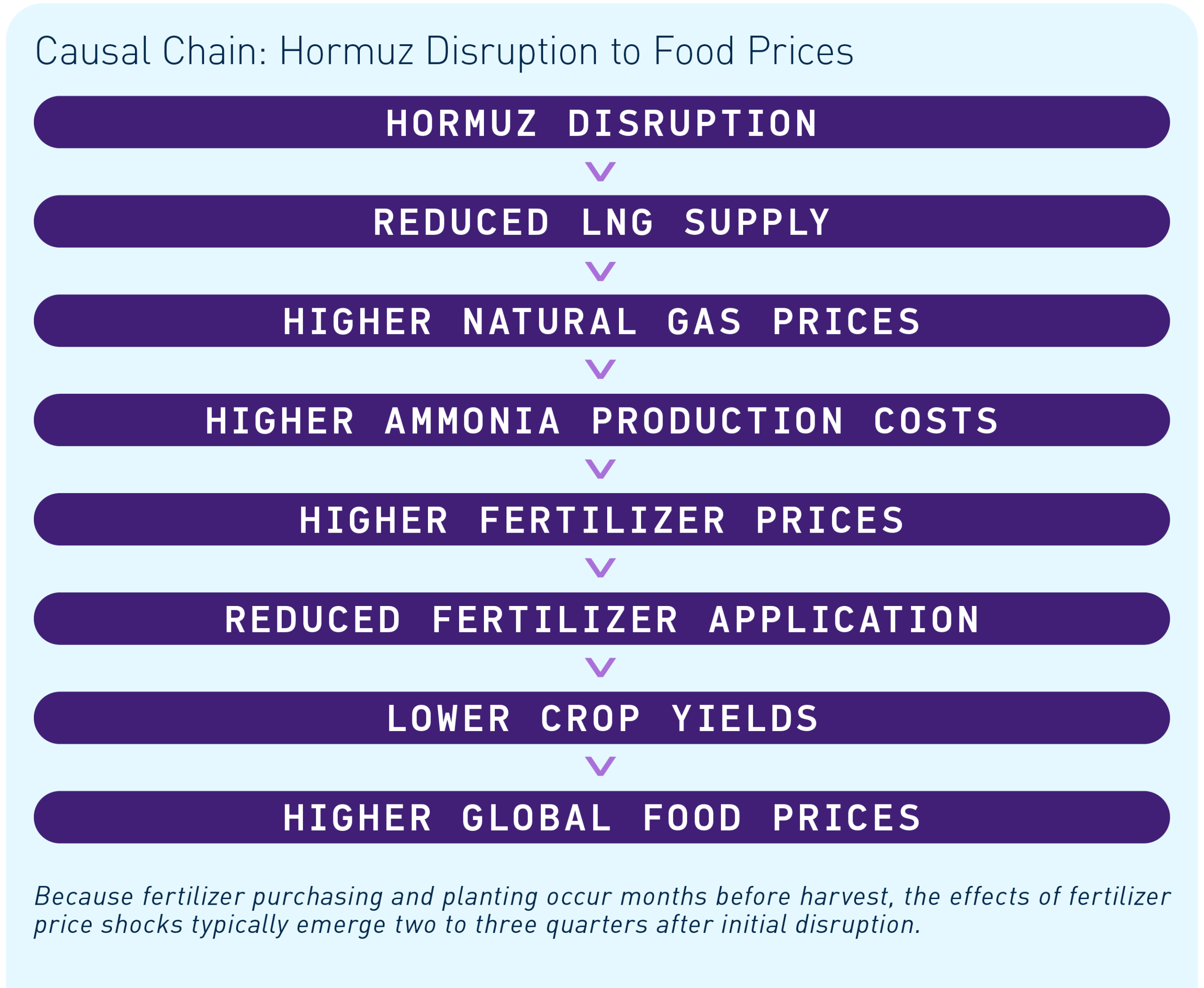

The fertilizer transmission channel and its long-term impact

With approximately 35 to 40 percent of the world’s fertilizer supply originating out of the Persian Gulf, one of the clearest second-order effects of a prolonged disruption runs through fertilizer production. Natural gas is the dominant feedstock used to produce ammonia, which is the foundational input for most nitrogen fertilizers used worldwide. The Strait of Hormuz is both one of the world’s most important energy chokepoints and a latent food-system chokepoint.

The transmission mechanism follows a straightforward chain:

Hormuz disruption

- reduced LNG supply or higher natural-gas prices

- higher ammonia production costs

- reduced fertilizer supply and increased fertilizer prices

- reduced fertilizer application by farmers

- lower crop yields

- higher global food prices

Agricultural cycles introduce a delay into this process. Fertilizer purchasing typically occurs months before planting seasons in the Northern Hemisphere. When fertilizer prices spike during this window, farmers often respond by reducing application rates rather than absorbing the full cost. The economic consequences of a maritime disruption may not become visible in food markets until two or three quarters later, when harvest yields reflect earlier input decisions.

International food security assessments have repeatedly shown that fertilizer price spikes translate quickly into higher staple food prices in import-dependent economies. The United Nations World Food Programme has identified several regions—particularly parts of East Africa, the Middle East, and South Asia—where agricultural productivity depends heavily on imported nitrogen fertilizers and rising input costs can translate into higher food insecurity. Countries such as Sudan, Yemen, Ethiopia, Somalia, and Afghanistan are especially sensitive to fertilizer and grain price shocks because of their dependence on imports and limited fiscal capacity to absorb higher food costs.

In these environments, food-price volatility carries implications beyond agricultural markets. Sudden increases in staple food costs can strain government subsidy programs, increase humanitarian demand, and exacerbate political tensions in already fragile states. Periods of sharp global food price increases have historically coincided with political instability in import-dependent regions, including during the 2007–2008 global food crisis and the 2010–2011 price spike that preceded unrest across parts of the Middle East and North Africa.

A parallel transmission channel runs through helium. Unlike with fertilizer, where the largest effects emerge with a seasonal lag, helium shortages tend to affect downstream users more quickly. Supply disruption can force immediate allocation decisions across semiconductors, MRI and other cryogenic medical uses, laboratories, aerospace, and specialty gases. Because these sectors rely on helium for processes that have few immediate substitutes, even short supply interruptions can affect research activity, medical imaging capacity, and high-technology manufacturing. In that sense, helium is a shorter-cycle example of the same stacked-constraints problem: disruption in a maritime corridor degrades an upstream input that critical sectors cannot easily substitute in the near term.

Disruptions in the Strait of Hormuz therefore propagate far beyond energy markets. Because natural gas, petrochemical feedstocks, and fertilizer intermediates share the same maritime corridor, sustained disruption in the strait can transmit simultaneously into industrial production, agricultural output, and food security. In this sense, the Strait of Hormuz is both an important energy chokepoint and a latent food-system chokepoint: a corridor where maritime instability can eventually surface as higher food prices, fiscal strain in import-dependent economies, and increased geopolitical volatility.

Freight, insurance, and the hidden constraint layer

Commodity supply is only one dimension of the risk. The global trading system also depends on a network of service providers—insurers, banks, ports, carriers, and classification societies—that enable goods to move across borders.

When geopolitical risk rises in a shipping corridor, these actors often respond faster than governments.

Operational consequences can include:

- higher war-risk insurance premiums

- tighter underwriting standards

- refusal to service vessels operating in higher-risk corridors

- increased documentation requirements for payments

- carrier surcharges and route changes

These measures rarely appear as formal trade restrictions; instead, they manifest as operational friction. Cargo still may move, but transit times become longer, costs rise, and delivery schedules become less reliable. For many companies, the immediate business impact is not scarcity but erosion of schedule reliability.

Chokepoint stacking

Most supply chains can absorb a single disruption through substitution, rerouting, or temporary buffering. The challenge arises when several constraint layers tighten simultaneously. Disruption in the Strait of Hormuz therefore interacts with other pressures already affecting global trade, including:

- heightened maritime enforcement targeting sanctions-evasion networks

- tightening export-control scrutiny and licensing throughput

- stricter documentation requirements from banks and insurers

- trade remedies affecting upstream industrial inputs

- instability in other strategic shipping corridors

When these pressures coincide, the system loses flexibility. Rerouting becomes harder, inventory buffers increase, and working capital requirements rise.

The result is rarely a single catastrophic breakdown but rather a persistent degradation of logistics reliability and cost structure.

What would change our call

Hostilities in and around the Strait of Hormuz have moved beyond geopolitical tension into active maritime conflict. Iranian forces and affiliated actors have targeted merchant shipping through both virtual and physical means, resulting in damage to commercial vessels and casualties among crews.

One potential response is commencement of naval escort operations to protect merchant traffic transiting the corridor. The United States’ current position is that European allies and other interested countries should provide the escorts while the US’s focus remains combat operations in Iran. However, those countries to date have, for myriad reasons, been reluctant to provide forces, rendering escort operations currently unlikely in the near term.

Even with naval protection, however, the key analytical question remains whether the conflict degrades commercial throughput across the corridor.

Several indicators would materially change our assessment:

- First, sustained attacks on escorted or nearby merchant vessels would indicate that naval protection is not fully restoring security for commercial shipping. If successful strikes continue despite escort operations, shipping companies and insurers may reassess the viability of routine transits.

- Second, the reaction of the maritime services ecosystem will be critical. If insurers impose prohibitive war-risk premiums, if major shipping lines suspend Gulf transits, or if ports and financial institutions begin applying broader risk exclusions, the corridor could become commercially constrained, even with naval escorts present.

- Third, shipping throughput will be the most important operational signal. Indicators such as declining tanker transits through the strait, vessel backlogs at Gulf export terminals, or large-scale rerouting of traffic away from the corridor would indicate that the system’s ability to move commodities reliably is degrading.

Finally, the risk profile will grow more severe if maritime pressure begins stacking across multiple shipping corridors simultaneously. Continued instability in the Strait of Hormuz alongside security risks in the Red Sea or capacity constraints in the Panama Canal would reduce global rerouting flexibility and increase the likelihood that localized conflict will evolve into broader supply-chain disruption.

In that scenario, the issue would shift from episodic maritime attacks to a structural constraint on the movement of energy and industrial commodities through the global trading system.

Bottom line

The defining feature of the current environment involves continued accumulation of constraints across the systems that move goods through the global economy, rather than a single geopolitical event.

Hostilities in and around the Strait of Hormuz have introduced direct maritime risk to commercial shipping. Naval escort operations by the United States and allied partners, if implemented, may help preserve the physical movement of vessels through the corridor, but they will not eliminate broader commercial pressures that determine whether trade continues to flow reliably.

Oil may dominate headlines, but LNG, petrochemical feedstocks, fertilizers, and refined fuels also move through the strait in significant volumes. Disruption in these flows can propagate through agriculture, manufacturing, transportation, and consumer markets, often with delays that only become visible several quarters after the initial disruption.

In import-dependent economies where food security is fragile, international food security assessments suggest that fertilizer price shocks can translate quickly into higher staple-food prices, rising humanitarian pressure, and increased political instability. Meanwhile, helium adds a faster-moving transmission channel into semiconductor, medical-imaging, laboratory, and aerospace markets—sectors where supply interruptions can affect critical research, healthcare, and high-technology manufacturing well before broader agricultural effects appear.

For executives and boards, the relevant question is not simply whether the strait closes outright. It is whether maritime risk, insurance restrictions, logistics friction, and commodity volatility begin to stack in ways that reduce the reliability of global trade flows.

Even in the presence of naval protection, the commercial system around shipping—insurers, carriers, ports, banks, and commodity buyers—ultimately determines whether throughput holds or deteriorates. Limiting exposure to the corridor likely will not result in a sudden halt in trade. Instead, we will see declining schedule reliability, longer lead times, higher working-capital requirements, and a greater likelihood of service disruption across supply chains.

The strategic risk is not simply conflict in a single maritime corridor—it is the loss of flexibility when multiple constraints tighten at the same time. As we discussed in our earlier analysis of stacked geopolitical constraints, the strategic issue is the cumulative effect of multiple pressures that reduce the system’s ability to sustain throughput.

References

Dunn, Candace, and Justine Barden, “Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint,” US EIA (June 16, 2025). https://www.eia.gov/todayinenergy/detail.php?id=65504

Garland, Max, “FedEx, UPS up fuel fees, levy Middle East surcharges amid Iran war,” Supply Chain Dive (March 13, 2026). https://www.supplychaindive.com/news/ups-fuel-surcharge-table-increase-2026/814187/

International Energy Agency (IEA), Ammonia Technology Roadmap (October 11, 2021). https://www.iea.org/reports/ammonia-technology-roadmap

Kumar, Arunima, Sumit Saha, and Toby Sterling, “Helium prices soar as Qatar LNG halt exposes fragile supply chain,” Reuters (March 12, 2026). https://www.reuters.com/business/energy/helium-prices-soar-qatar-lng-halt-exposes-fragile-supply-chain-2026-03-12/

Miglierini, Julian, Martin Rentsch, Shaza Moghraby, and Rene McGuffin, “WFP projects food insecurity could reach record levels as a result of Middle East escalation,” UN World Food Programme (March 17, 2026). https://www.wfp.org/news/wfp-projects-food-insecurity-could-reach-record-levels-result-middle-east-escalation

Qatar Energy, “Ras Laffan Helium.” https://www.qatarenergylng.qa/english/Operations/Ras-Laffan-Helium

Stroh, Kelly, “How the Iran conflict is impacting global ocean shipping flows,” Supply Chain Dive (March 11, 2026). https://www.supplychaindive.com/news/iran-conflict-global-ocean-shipping-flows-lars-jensen-tpm26/814250/

US Geological Survey, “Helium,” Mineral Commodity Summaries (January 2026). https://www.usgs.gov/centers/national-minerals-information-center/helium-statistics-and-information

UN Conference on Trade and Development, Strait of Hormuz Disruptions: Implications for Global Trade and Development (March 10, 2026). https://unctad.org/system/files/official-document/osgttinf2026d1_en.pdf

US Energy Information Administration (EIA). https://www.eia.gov/international/analysis/special-topics/World_Oil_Transit_Chokepoints

Related Industries

Prepare for what's next.

ThinkSet magazine, a BRG publication, provides nuanced, multifaceted thinking and expert guidance that help today’s business leaders adopt a more strategic, long-term mindset to prepare for what’s next.